Amex Raises Merchant Acquiring Threshold to 3 Million: What Your Business Needs to Know

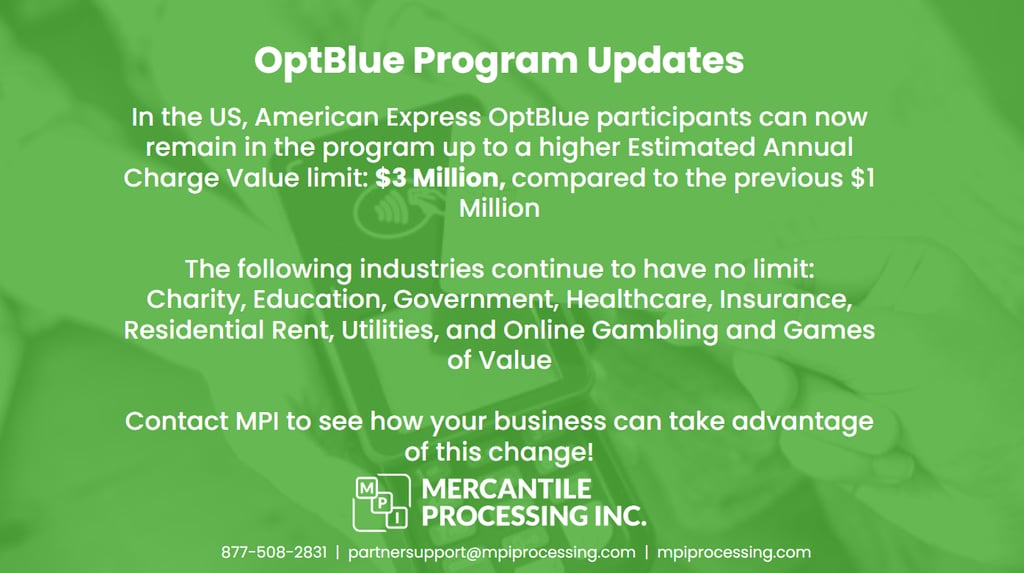

American Express has announced a significant update to its OptBlue program that will impact merchants and payment processors alike. Effective April 17, 2026, American Express has increased its OptBlue merchant acquiring ECV threshold to $3 million.

Kyle Morgan

6/15/20262 min read

American Express OptBlue Program Update for 2026

American Express has announced a significant update to its OptBlue program that will impact merchants and payment processors alike. Effective April 17, 2026, American Express has increased its OptBlue merchant acquiring ECV threshold to $3 million. This change creates new opportunities for businesses that were previously in the $1-2 million range.

What is the OptBlue Program?

OptBlue is the American Express program that allows qualified payment processors and merchant service providers to directly acquire and service eligible American Express merchants. Instead of merchants needing a direct American Express relationship, they can receive American Express acceptance through their payment processor.

Industries With No ECV Threshold

The following industry categories continue to have no OptBlue volume limitation:

Charity

Healthcare

Education

Government

Insurance

Residential Rent

Utilities

Online Gambling and Games of Value (subject to certification requirements)

Certain Merchant Category Codes (MCCs) within these industries may still have additional eligibility requirements.

Why This Matters for Businesses

The increased threshold allows more growing businesses to remain within the OptBlue ecosystem while benefiting from:

Simplified American Express acceptance

Flexibility to stay with Existing Payment Processor Longer

Unified funding and reporting

Streamlined customer support

Reduced administrative complexity

For businesses approaching $1 million, $2 million, or even $3 million in annual American Express volume, this update provides additional flexibility before alternative acquiring arrangements may be required. Even above $3 million, the fees on OptBlue can be less that AmexDirect, so this change can be meaningful.

Frequently Asked Questions (FAQs)

What is the cap on the Amex OptBlue program?

As of April 17, 2026, the cap for the merchant acquiring fee for Amex OptBlue is $3 million.

Will the April 2026 OptBlue program update change my processing rates?

Rates will not change after the April 2026 change. It simply expands eligibility of the program to more merchants.

Does this change affect chargebacks or dispute handling?

No. American Express disputes and chargeback procedures remain in place. However, OptBlue merchants generally work through their processor for support and dispute management.

What is the difference between Amex OptBlue and Amex ESA?

Amex ESA is American Express’ direct payment processing program. Merchants over $3 million are generally required to use ESA. Amex OptBlue is a program that allows small and mid-sized businesses to accept Amex cards through a third party payment processor.

I have a branded hotel (e.g. Hilton, Hyatt), do I have to process through AmexDirect?

Most major hotel brands have corporate discount programs with Amex, meaning going through ESA is not necessary. You can use any standard payment processor.

I’m a sales rep who sold an account using ESA. Do I need to redo the contract to take advantage of the new OptBlue changes?

No, the change from Amex ESA to OptBlue can be made quickly and easily, with minimal paperwork.

How MPI Can Help

Here at MPI, we pride ourselves on our “local” feel. If you are a business who is affected by this change, or just looking for a new payment processor, contact us at partnersupport@mpiprocessing.com.